The Mathematical Masterpiece: The Kelly Criterion in Sports Speculation

In the entire mathematical catalog of optimal capital growth under conditions of uncertainty, no single theorem holds the revered status of the Kelly Criterion. Developed not for Wall Street or Vegas, but inside the elite laboratories of Bell Telephone in 1956, this formula represents the definitive, mathematically proven method for maximizing the expected logarithm of wealth over a series of wagers.

To the serious analyst, the Kelly Criterion is the essential bridge between Alpha identification (knowing you have an edge) and Capital allocation (knowing how much to bet). If you bet too little, you waste your edge and leave compounding growth on the table. If you bet too much, you encounter the inescapable mathematical reality of ruin-meaning that even if you win 99% of the time, your eventual bankruptcy is guaranteed. The Kelly Criterion identifies the absolute optimal geometric peak between these two extremes.

1. The Historical Paradigm: From Signal Processing to Wealth Extraction

The formula owes its existence to John L. Kelly Jr., a brilliant Texan physicist working alongside information theorist Claude Shannon at Bell Labs. Kelly’s initial academic focus was not gambling; he was attempting to solve a physics problem regarding signal noise in telephone circuits. He wanted to know how much information could be reliably transmitted through a static-heavy channel.

Kelly realized that the exact same mathematical frameworks governing data transmission could be applied directly to the extraction of wealth from horse racing and sports betting. If an observer possesses "private information" (or "inside information") that makes their estimate of an outcome more accurate than the public market consensus, they have established a "clean signal" amidst market noise. The Kelly Criterion is simply the algorithm designed to calculate the precise volume of capital to route through that signal to maximize terminal wealth.

2. Deriving the System: The Foundational Formula

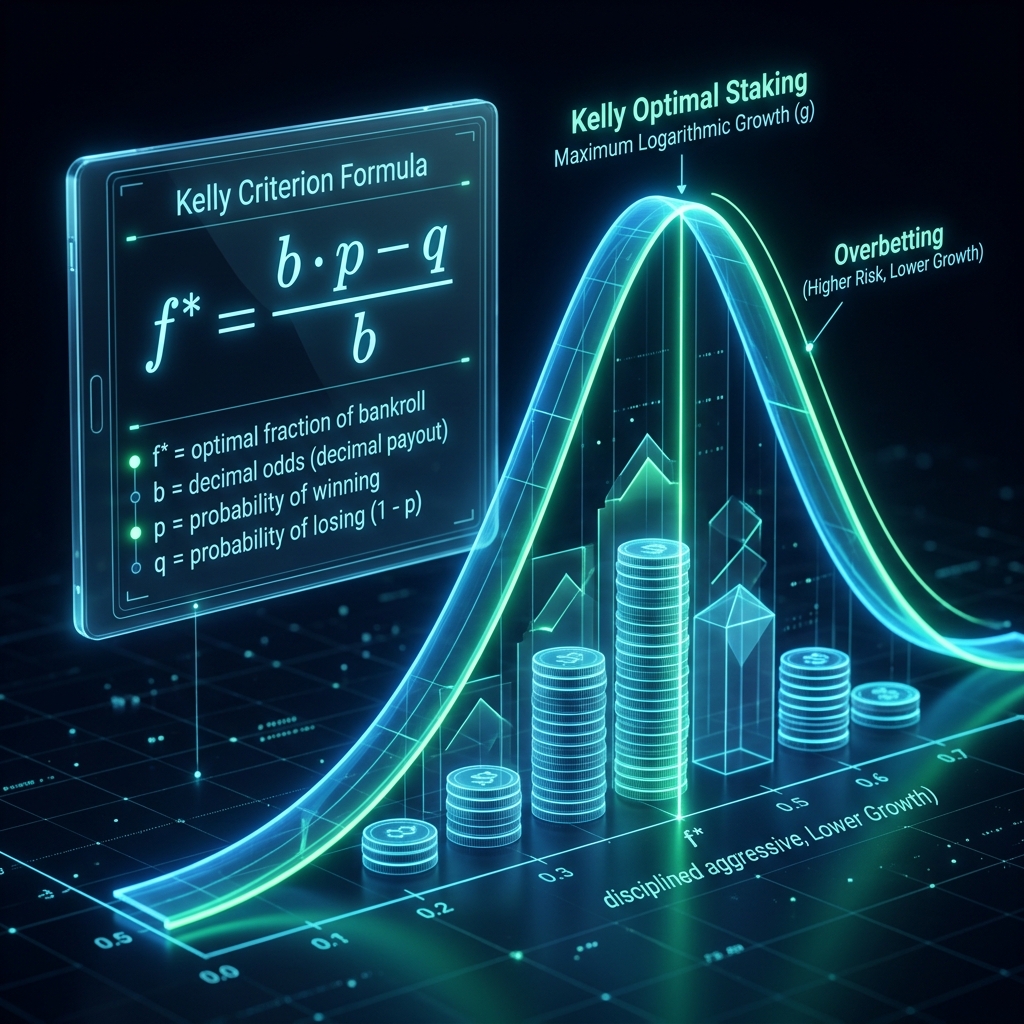

The standard Kelly Criterion for a single-outcome wager is expressed through the following elegant algebraic fraction:

f* = (b * p - q) / b

Let us define the structural components of this equation:

- f* (Fraction): The optimal proportion of your active current bankroll to wager on the event.

- b (Decimal Odds Ratio): The net fractional odds received on the wager. This equals the

Decimal Odds - 1(e.g., at +150 / 2.50 odds, b = 1.50). It is the profit returned per dollar risked. - p (Win Probability): The true, objective probability of the wager winning.

- q (Loss Probability): The probability of the wager losing. Since the event is binary,

q = 1 - p.

The numerator of this equation, (b * p - q), represents the Edge. If this numerator is zero or negative, the formula outputs an f* of zero or less. Mathematically, the Kelly Criterion strictly mandates that you should never wager capital on an event where you do not possess a positive edge, regardless of the payout.

3. Executing the Calculus: A Practical Application

Let us observe a real-world scenario using a $10,000 bankroll. An analyst identifies an NBA spread priced at +120 (2.20 Decimal) where the true win probability, verified by a high-precision Monte Carlo simulation model, resides at 50%.

- Determine Odds Ratio (b): 2.20 - 1 = 1.20.

- Determine Win Prob (p): 0.50.

- Determine Loss Prob (q): 1 - 0.50 = 0.50.

Plug these values into the Kelly Formula:

f* = (1.20 * 0.50 - 0.50) / 1.20

f* = (0.60 - 0.50) / 1.20

f* = 0.10 / 1.20 = 0.0833 (8.33%)

To maximize your bankroll's long-term exponential growth, the Kelly Criterion dictates that you should wager exactly 8.33% of your total capital ($833.00) on this specific +120 line. This represents the mathematical sweet spot: any less, and you compound more slowly; any more, and the increased volatility begins to drag down your long-term geometric mean.

4. The Double-Edged Sword: The Asymmetry of Risk

The full Kelly formula is theoretically perfect, but practically volatile. It assumes three absolute conditions that rarely exist in the real world:

- You possess an absolutely perfect, 100% accurate win probability (p).

- You have an infinite timeframe to allow the Law of Large Numbers to play out.

- Your bankroll is perfectly divisible (no minimum bet sizes).

In reality, if an analyst overestimates their edge by even a slight margin, placing a "Full Kelly" bet becomes catastrophic. If the formula tells you to bet 10%, but your model contains bias and your true probability is actually lower, you are now betting in what is known as the Over-Betting Zone.

The mathematical growth curve of the Kelly Criterion is highly asymmetric. Over-betting is exponentially more dangerous than under-betting. Betting exactly 2x the optimal Kelly amount results in an expected geometric growth rate of exactly zero, with an eventual 100% certainty of complete bankruptcy (Risk of Ruin). Because the penalty for over-betting is financial death, professional analysts almost never deploy Full Kelly stakes.

5. The Armor of Sub-Optimality: Fractional Kelly Sizing

To mitigate the violent volatility and protect against model error, professional syndicates Use Fractional Kelly Sizing. By scaling the output of the Kelly formula down by a static divisor-typically Half Kelly (0.50) or Quarter Kelly (0.25)-the operator achieves spectacular safety with very little performance sacrifice.

Consider the extraordinary efficiency of Quarter Kelly (betting 25% of the Kelly recommendation):

- Volatility Reduction: By betting only 25% of the Full Kelly size, your expected drawdown (the worst-case bankroll dip) is reduced by roughly 75%. The ride becomes dramatically smoother.

- Growth Preservation: Despite only risking 25% of the capital, you still capture 75% of the theoretical maximum growth rate. You forfeit 25% of the absolute peak performance in exchange for a bulletproof defense system against bankruptcy.

- Model Error Safety Buffer: If your statistical model overestimates your true probability by 10% or 20%, you still reside safely in the under-betting zone, far away from the cliffs of ruin.

6. Multivariate Kelly: Simultaneous Wagers

A common challenge occurs when you identify multiple +EV opportunities that are starting simultaneously. If you have 5 games kickoff at 1:00 PM EST, and the individual Full Kelly calculations for each game add up to 60% of your bankroll, you face massive correlation and liquidity risks.

Executing independent Kelly stakes concurrently is mathematically incorrect, as it assumes each bet resolves before the next is placed. To calculate optimal sizing for simultaneous, independent events, professionals Use a Normalized Simultaneous Kelly approach. One simple and robust method is to reduce the overall fractional scale based on the number of active bets, or more formally, to run a quadratic optimization algorithm to maximize the joint expected logarithmic return. For the retail trader, simply switching to an aggressive fractional model (like 1/8th Kelly) during high-volume schedules provides a natural and statistically sound safety valve.

Conclusion: Disciplined Aggression

The Kelly Criterion is not a conservative strategy; it is a formula designed for aggressive, orderly capital growth. It completely removes emotion from the equation, ensuring you bet big when your edge is deep, and retreat instantly when your edge evaporates. By applying the Kelly equation through a protective fractional lens, you equip your portfolio with a dynamic, self-correcting mechanism that automatically contracts your risk during downswings and expands it aggressively during upswings. It is the ultimate tool for transforming localized analytical insight into permanent, compounding financial power.